For more vital details, take a look at the FHA's lending limits in your state. Usually, FHA mortgages feature an additional insurance coverage charge called a "home mortgage insurance premium." Due to the fact that FHA loans are common and have lower deposit and credit report requirements, they are one of the most available home loan.

In addition, FHA loans enable a non-occupant co-signer (as long as they're a relative) to assist borrowers certify. Historically, the requirements for FHA mortgage insurance have varied over the years. Presently, an FHA loan requires both an up-front home mortgage insurance coverage premium (which can be funded into your loan amount) and month-to-month home mortgage insurance coverage.

The U.S. Department of Veteran Affairs supplies loan services to members and veterans of the U.S. military and their families. If you are eligible , you might qualify for a house loan that requires no down payment or month-to-month home loan insurance. VA home loans are created to help veterans buy houses with no deposit.

Comparable to FHA loans, the government does not straight issue these loans, instead they are processed by banks or personal lending institutions and ensured by the VA - mortgages or corporate bonds which has higher credit risk. While VA loans are attractive because they generally require no deposit, they don't have an optimum limitation, depending upon eligibility. Veterans, active-duty service members, and enduring spouses are eligible for VA mortgage loans.

Rumored Buzz on Find Out How Many Mortgages Are On A Property

These loans are fantastic to get individuals in homes, however are just offered to veterans. FHA 203k loans are home restoration loans for "fixer-upper" properties, assisting house owners finance both the purchase of a home and the cost of its rehab through a single mortgage. Existing property owners can likewise get approved for an FHA 203k loan to finance the rehab of their existing home.

5% down. An FHA 203k loan does not need the area to be presently livable and it has credit rating requirements comparable to routine FHA loans, however some lending institutions may need a minimum credit history of 620 to qualify. what is a non recourse state for mortgages. Numerous types of restorations can be covered under an FHA 203k loan: structural repairs or changes, modernization, elimination of health and wellness risks, replacing roofings and floors, and making energy conservation improvements, among others.

And they only require a 3. 5% deposit. what do i need to know about mortgages and rates. These loans require you to receive the worth of the property plus the expenses of any planned restorations. Both adhering and non-conforming home mortgages are types of conventional mortgages. A conforming loan satisfies specific guidelines established by the Federal Housing Finance Agency (FHFA) and Fannie Mae and Freddie Mac, however they are not insured by the federal government.

Since 2020, the adhering loan limitation is $510,400 in the majority of the U.S. and goes up to $765,600 in specific higher-cost areas, and is changed yearly. Conforming loans use much better rate of interest and donovanmssy992.cavandoragh.org/getting-the-what-are-all-the-different-types-of-mortgages-virginia-to-work lower charges than non-conforming loans. Adhering loans may have lower rates of interest and charges than non-conforming loans.

The 6-Minute Rule for How Do Reverse Mortgages Work In Utah

Non-conforming loans are loans that fall above the conforming loan limit set by the FHFA. There are several various types of non-conforming loans. The most typical is a jumbo loan. A jumbo loan is a loan that surpasses the conforming loan limitation. Due to the size of the loan, the requirements to certify are more strict.

Rate of interest can likewise be greater for jumbo loans since they are thought about more dangerous to the loan provider. Other kinds of non-conforming loans exist for borrowers with credit rating on the lower end, or borrowers with a high debt-to-income ratio. Those wanting to fund a costly residential or commercial property purchase will likely have little choice but to utilize a jumbo loan.

Jumbo loans can assist qualified borrowers purchase pricey homes. Getting approved for a jumbo loan might have more stringent requirements or extra fees. Each homebuyer is distinct, so taking the time to totally comprehend the process of selecting the best home loan for your needs is an important initial step. Ready to do some window shopping? SoFi provides home mortgages with competitive rates, a fast and easy application, and no hidden costs.

SoFi Home Loans are not offered in all states. See SoFi. com/eligibility for more information. Numerous factors affect your credit history and the rates of interest you may get. SoFi is not a Credit Repair work Organization as specified under federal or state law, consisting of the Credit Repair work Organizations Act. SoFi does not provide "credit repair" services or recommendations or support relating to "reconstructing" or "enhancing" your credit record, credit history, or credit ranking.

Which Banks Are Best For Poor Credit Mortgages Things To Know Before You Buy

The details and analysis supplied through links to third party sites, while thought to be precise, can not be guaranteed by SoFi. Hyperlinks are provided for informative functions and ought to not be deemed an endorsement. SoFi loans are originated by SoFi Loaning Corp (dba SoFi), a lending institution licensed by the Department of Financial Protection and Innovation under the California Funding Law, license # 6054612; NMLS # 1121636 .

Purchasing a home is arguably the most crucial purchase that you'll ever make, which is why it is essential to make the ideal choice. Offered the high expenses of a real estate purchase, the chances are that you will need to secure a house mortgage loan. While the fundamental property of all mortgages is the same (you'll be utilizing your brand-new home as collateral for a loan that allows you to acquire the home), there are lots of various options at hand.

No 2 individuals are the same, especially when it concerns purchasing a home. As such, banks and lending institutions offer various home loan products in order to serve the various requirements of a diverse market. Understanding the finer details of the contrasting home mortgage types ultimately allows you to pick the most ideal path for buying your property.

Residential or commercial property rate The right home loan for a $100,000 loan may not be the very best option for a $1,000,000 home loan. Loan-to-Value ratio When the deposit is a significant portion (over 50%) of the property price, a particular home loan type may be better. Debt-to-Income ratio Banks factor in your other debts versus your revenues to guarantee that you can making payments and your scenario can influence which alternative is best.

The 10-Minute Rule for What Percentage Of Mortgages Are Below $700.00 Per Month In The United States

Credit rating Credit history are another prominent factor that can affect the overall repayment structure. Other aspects, such as the duration of the home loan, will also affect the scenario. By comprehending the various home loan, it's possible to discover a service that suits your budget and situation to produce the most affordable general repayment.

After all, the contrasts between one lender and the next can be substantial. Nonetheless, the mortgage type will constantly supply the structure for making the ideal choice. While there are other mortgage types available, specifically if you're wanting to end up being an investor or property owner, mortgage are broken timeshare vacation into 7 main categories.

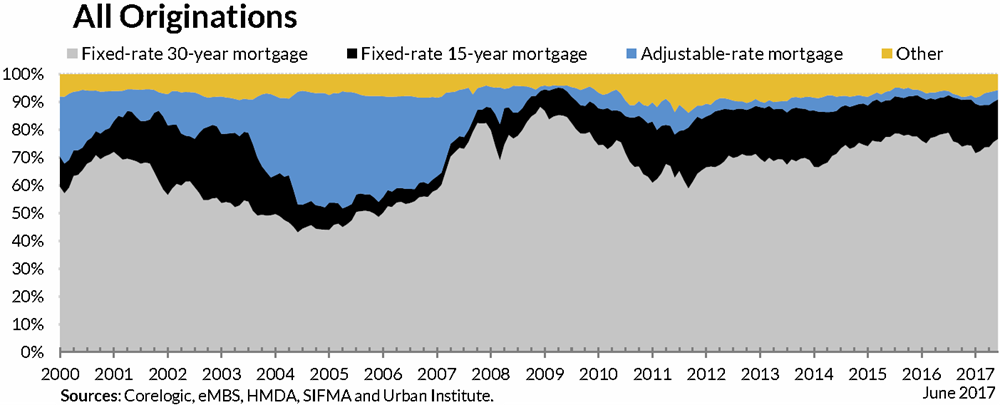

It is an arrangement in which your payments and rates of interest are set at a guaranteed level throughout the period of the loan. Additional reading This makes the financial management aspects of the home loan far easier to control. The regard to the arrangement can be individualized to suit individual requirements based on monetary status and individual preference.